As stated in previous articles, I have a combination of experiences that don't seem to go well together at first glance. I have always been interested in public markets, I have a cybersecurity degree (and am working on an engineering one), I studied China in grad school and lived in Taiwan for almost two years. How do I make these unrelated skillsets, each lacking sufficient depth in their respective domains, work together?

I have also been watching the AI buildout with keen interest. Lately, I started reading SemiAnalysis for their highly technical, plugged-in takes on the global semiconductor industry. I couldn't help but navigate to their job listings and I noticed they were looking for a China analyst.

Why wouldn't they be? China is the "pacing threat," per the US government. Our supply chains are deeply intertwined, and it is our nearest strategic competitor in the fast-evolving realm of AI. The conventional wisdom is that it is anywhere from a few years behind the US to only a few months. The reality is that this figure is a moving target and it deserves constant scrutiny. That's where I got the idea to write a practice piece for the blog. I would work my magic with my trusty partner, Claude Code, produce some high-impact intelligence, and Dylan would soon be calling me up to throw money at me. If only it were that easy.

During our brainstorm session, Claude laid out several different avenues of attack. A very promising one was with respect to CloudMatrix 384: a behemoth of a compute cluster that uses Chinese NPUs (8x Ascend 910C per server x 48 servers) and optical interconnects to train and run models. We had zeroed in on the efficacy of optical modules versus copper, benchmarked the failure rates, and set out to predict when they might start to alleviate. But the enormity of the task made it clear that my first practice piece would take several weeks of research to land, bottlenecked by the gap I need to fill in general understanding of Chinese market dynamics. That piece is still on its way, but in order to secure a more frequent launch cadence, I narrowed the scope of the endeavor. I decided that combing through individual documents — whether that be a financial disclosure, a government policy, or conference minutes — one at a time, from top to bottom, and translating it for a Western audience. Hence, the new series Decoding China was born. We will start with Zhongji Innolight (中际旭创, ticker 300308.SZ), one of two dominant suppliers of the 800G optical transceivers Nvidia ships inside its AI systems to interconnect GPUs across racks. Their most recent disclosures include the FY2025 annual report and the Q1 2026 quarterly, both filed on cninfo.com.cn under ticker 300308. What follows is our attempt to extract the actionable signal.

Bottom Line

This is a company that is absolutely printing money. Innolight is a beneficiary of hyperscaler capex in the same way that Micron and SanDisk are, and its stock price is behaving accordingly. However, a Sword of Damocles is hanging over its head. The company is on a collision course with a new product stack that threatens to kill its golden goose. It is not, however, passively awaiting this fate. Below, we will look at the tech, the dangers, and the company's mitigation efforts.

What do they do?

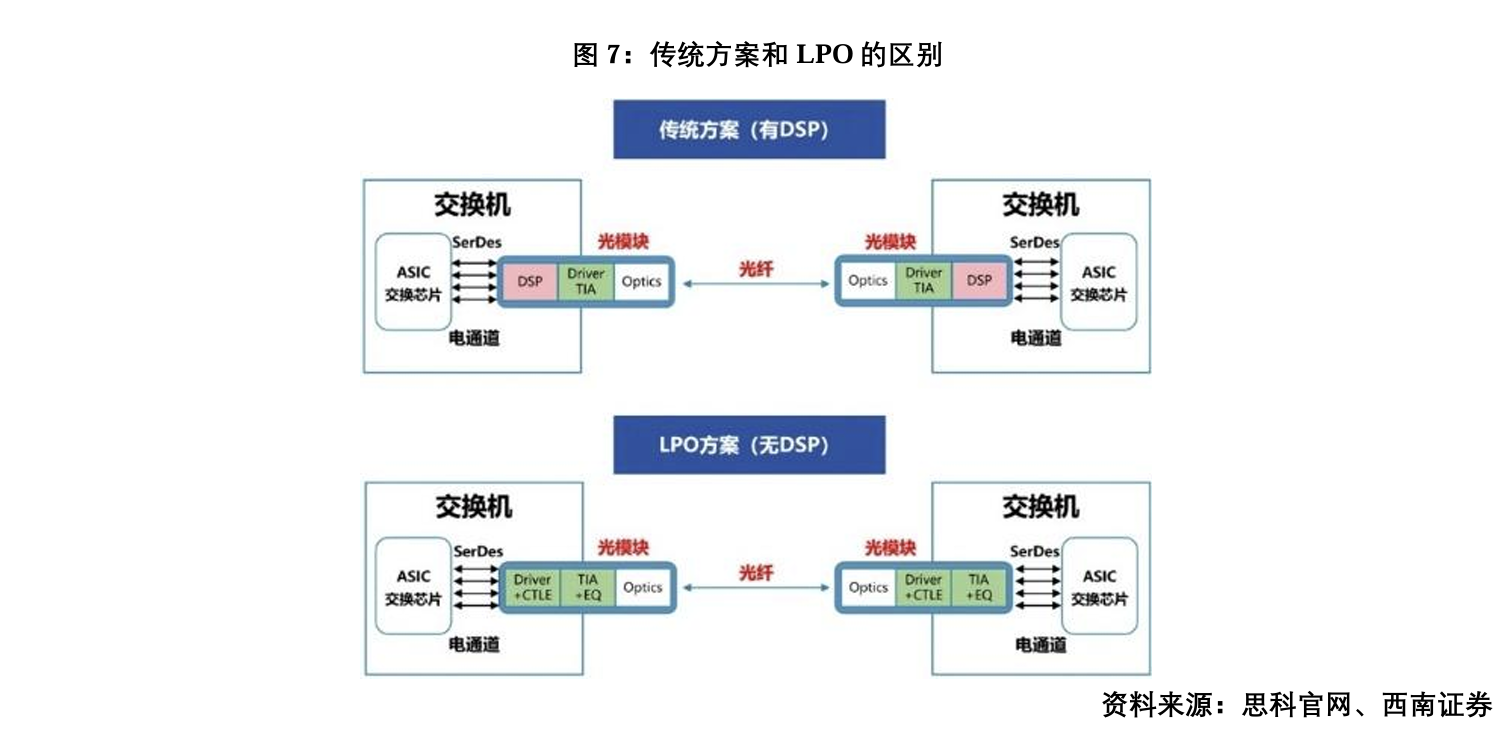

Zhongji Innolight is an integrator of pluggable optical modules. These products sit between a server (or switch) and the fiber-optic cable that connects them, where they translate electrical information into light (and back). Fiber carries advantages vis-a-vis copper, but it adds the translation burden. If you want to use fiber, you have two main options: traditional, which comes with a DSP (Digital Signal Processor), or LPO (Linear Pluggable Optics), which contains no DSP. Traditional modules are higher power, higher cost, and higher fidelity. LPO is cheaper and consumes about 60% less power, but you will pay for it with a higher error rate. That's an oversimplified bird's-eye of the main idea.

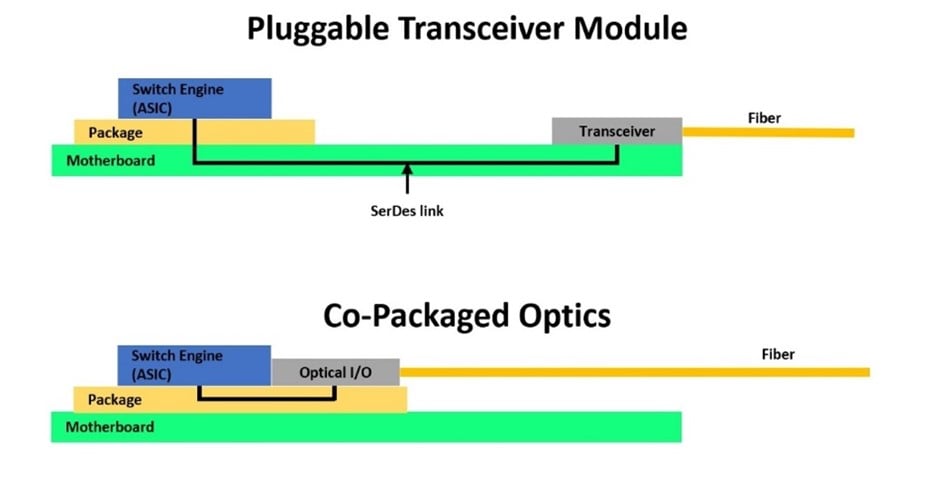

Innolight traffics in both types of modules. But there is a third on the horizon that's the game-changer, CPO (Co-Packaged Optics). CPO comes, as its name would suggest, co-packaged onto the same module as the switch/accelerator ASIC. It performs the electrical-optical translation millimeters away from the chip itself, removing the need for that translation to happen inside the pluggable. This represents an existential threat to Innolight's core product.

At this point, it's worth getting a little deeper into the different types of pluggables so that we can better frame the CPO threat. The differences sit across a few different axes. The first one is the DSP/non-DSP axis already outlined. The second is transfer speed, for which Innolight offers anywhere from 100G (that is 100 gigabits per second) to 1.6T and soon will offer a 3.2T version. A third fundamental dividing line is how the modules are assembled. Innolight offers either of two platforms: discrete and silicon photonics (SiPh). The discrete platform contains four components that are needed to perform the electrical-optical translation, a modulator, a photodetector, waveguides, and a laser. These components are sourced from suppliers, assembled by Innolight, and sold as a unit. The SiPh platform bundles everything but the laser into an integrated photonic chip that Innolight develops in-house and has fabbed at an outside foundry (Tower Semiconductor is the most-cited). This distinction will become crucial later as the silicon photonics architecture is essentially exactly how CPO works, just inside the pluggable module as opposed to integrated with the ASIC.

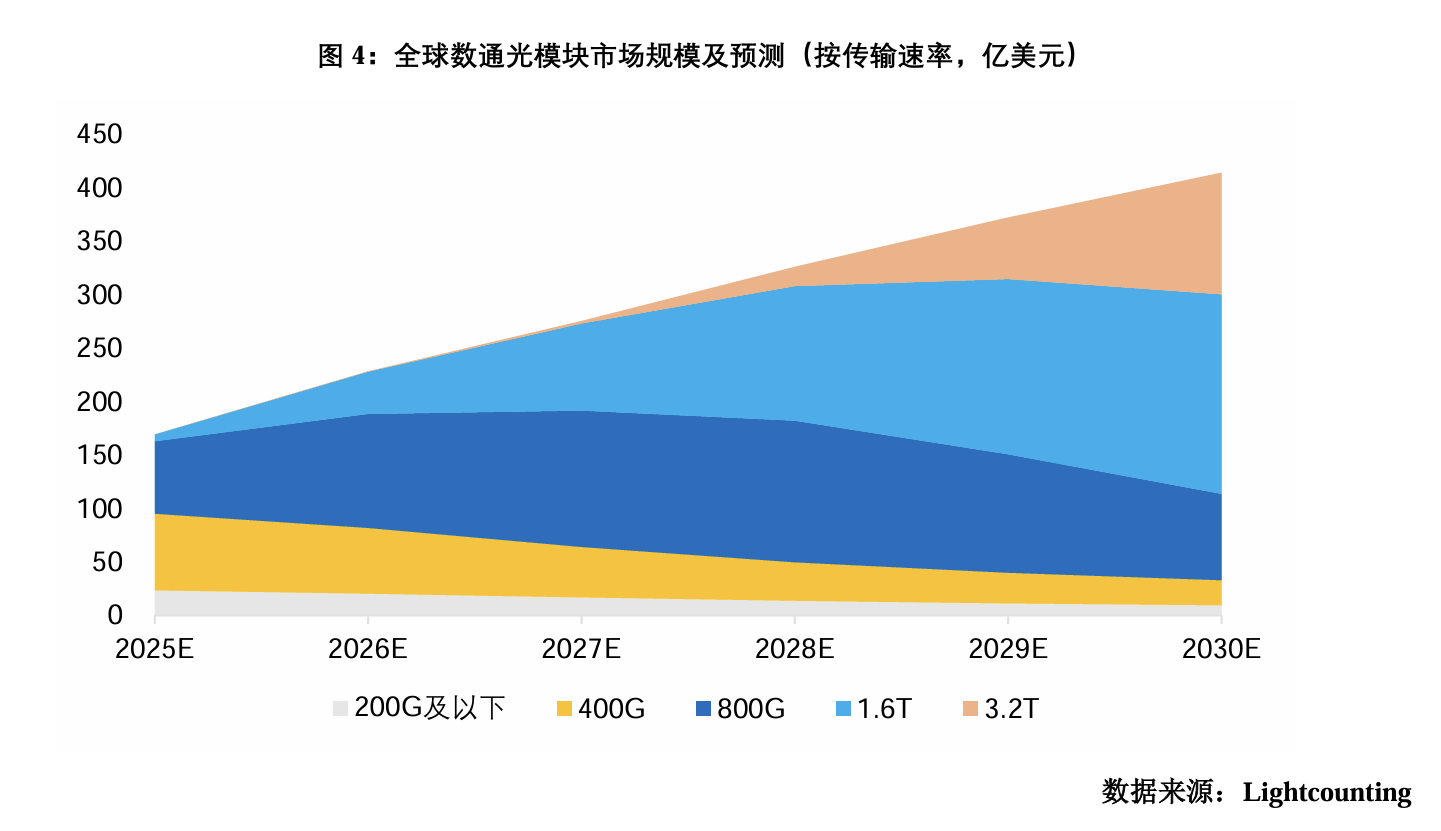

CPO tech is proven but not yet ubiquitous. Innolight believes it still has years of runway to sell their pluggables, and its aggressive investments back that up. The annual report is silent on how long until CPO disrupts their business model, but projects total demand for their 800G, 1.6T, and 3.2T modules to grow until 2030 (data courtesy of Lightcounting).

By the numbers

For the time being, the earnings are real. The 2025 report showed revenue up 60% YoY to $5.35B and profits up 108% YoY to $1.51B. To show just how fast this is accelerating, compare those numbers to 1Q26, up 192% and 262% (!), respectively, from 1Q25. Furthermore, there were several indications throughout the documents that those earnings are of a high standard of quality. First, almost the entirety of earnings are from recurring sources, meaning none of it is buoyed by windfalls, such as subsidies or asset sales. Second, nearly all of it is cash in the bank, not IOUs. Operating cash flow ≈ net profit ≈ $1.5B. Finally, there are no accounting tricks that make earnings look better than they are. Of their R&D expenditures, a low-and-falling portion of it is being amortized across time. This means that they write the majority of their investments off as losses, and the profits are what's left over after.

Where the numbers lead, management is following. They are not acting like this is a business in danger of decline. In 1Q26, cash spent on fixed-asset capex was up 381% against 1Q25 to $270M. The balance sheet shows construction in progress (CIP) assets sitting at $330M, up from $199M at the end of 2025, a 66% increase in 3 months. They are funding this expansion almost entirely out of operating cash while still managing to grow the pile from $0.98B in 1Q25 to $1.71B a year later. The signal is clear. They are not taking the profits from the data center gold rush and stashing it for a rainy day. They are plowing it right back into the business, which suggests that supply cannot keep up with current demand, and that demand will be there for years to come.

Dangers

But quality does not mean safe. The numbers, while impressive, are precarious. The business model is exposed not only to the CPO threat, but also to offshore dependence, customer/supplier concentration, macro trade conditions, a tax technicality, and forex drag. Let's get into each one.

The most asymmetric figure in the entire FY25 report is Innolight's exposure to international markets. Of their $5.35B in revenue, $4.84B (~91%) comes from overseas. The document mentions heavy reliance on North America and Europe, and states explicitly that parts for everything but the lowest-speed modules (below 200G) cannot be produced domestically. The supply chain is extremely vulnerable to both upstream and downstream disruptions.

Likewise, both customers and suppliers are less than ideally diversified. Innolight's top 5 customers represent 76% of revenue, a number that gets worse when we find out who customer E likely is (more on that below). The single top customer by revenue is responsible for 24% of the headline number. As for suppliers, the top 5 total 52% of expenditures, the largest of which clocks in at 36% alone. Any change in business posture from either of these high-value relationships alters next year's numbers materially.

Innolight explicitly mentions a potential escalation of reciprocal tariffs as a specific danger. Obviously, being as exposed to international markets as it is, a trade war between the US and China would bring about serious pain for Innolight.

Speaking of international trade, foreign exchange fees have escalated and represent a persistent drag on profits. In 2025, total forex losses were $44M. In the first three months of 2026, they spent $35M — on track to >3x 2025.

Lastly, an interesting tidbit about tax eligibility could turn out to be not quite a mortal wound, but an annoying and unnecessary cost to the company which investors should be aware of. In China, high-tech companies get a favorable 15% tax rate but have to recertify every 3 years. Innolight's subsidiaries are due to recertify at varying intervals, with the earliest around 2027. The report warns that if it or any of them fail to obtain this classification for any reason, its tax rate could jump to 25% overnight, resulting in additional costs.

Customers are more concentrated than they look

This was a spectacular catch by Claude. Chinese financial reports anonymize their customers and suppliers, reporting as Customer/Supplier A-E next to the dollar amounts and percentage of revenue or expenses. While we don't know for sure who is who, there are certain things we can infer. For example, Customer A at 24.06% might be Nvidia or another hyperscaler. Supplier A is probably either Marvell or Broadcom, given that the most expensive component of an optical module is the chip inside. But there is one coincidence that gives us a high degree of confidence in the identity of Customer E.

The revelation is that of the top 5 customers, at least one is highly likely to be a subsidiary of Innolight itself. On page 66 of the annual report, there is a line for disclosure of Related Party Transactions. The only entry is for a company called Pinewave with ~$433M worth of transactions. In the report, this value is given in USD while revenue by customer is in CNY, but if you apply the conversion, the dollar value lines up almost perfectly with none other than Customer E at 8.1% of all revenue. If Innolight's fifth largest customer is its own subsidiary, that makes the customer concentration risk worse than it already appears.

Mitigation efforts

This is where it gets interesting. Innolight's management team is keenly aware of the dangers outlined above (they wrote it first). The prescription is to internationalize. Diversifying across borders shields Innolight from single points of failure. To that end, the company has spawned a handful of subsidiaries as well as taken on some notable investors.

Let's start with the investors. The report describes approving a $517M capital raise paid in part by two new shareholders: Platinum Orchid B 2018 RSC Ltd. and Temasek Holdings, sovereign wealth funds for the United Arab Emirates and Singapore, respectively. One caveat is that as of 1Q26, the action has still not been finalized in cash.

Another notable foreign investor with name recognition is none other than Morgan Stanley. As of the 1Q26 report, MS took a direct stake (distinct from the consolidated foreign investment vehicle, HKSCC) of about 6.5M shares, or 0.58% of the company, making it a named top-10 shareholder.

Innolight is also expanding its footprint around the world. In 2025, it stood up a total of 9 subsidiaries across China, Singapore, Thailand, and the United States. Singapore is home to Terahop (67% owned by Innolight), Pinewave (59% owned by Terahop), Vincrest, and Lunaris. In Thailand, there are Terahop Thailand and Picmore. As near as we can tell, Singapore is the sales & management hub and public-facing face of the network while Thailand is the manufacturing backup. In the US, there are Terahop Holdings and Terahop Photonics.

Lastly, we couldn't help but notice that a new board member has begun his term last year as well — a Canadian. Yan Zhuang went to the University of Alberta and worked the Far East for Motorola and Canadian Solar, among others. He is currently the CEO of CSI Solar Co., Ltd, the operating subsidiary of Canadian Solar, and a PRC resident.

What about CPO?

Innolight is conspicuously silent in its reporting about efforts to stay relevant in the coming era of CPO. Still, there are a few hints in the document that allow us to make some assumptions. Here we will explore what Innolight is likely doing to stay ahead of the curve and why that may not be enough.

As we explained above, Innolight's current SiPh platform, in production since 2023, is already half way to a CPO — but the second half is much harder. Innolight is fundamentally not a provider of entire servers, and the full stack can only be put together by companies like Broadcom and Nvidia. The document repeatedly references continued investment in SiPh, preserving Innolight's leadership status, and solidifying its advantage in foreign markets. From this we infer that Innolight plans to stay in the SiPh business long after CPO has arrived — though we can't say how.

The company holds a cumulative 411 patents, of which 215 are invention patents. Its President, Liu Sheng, himself holds a PhD from Georgia Tech and previously worked as an R&D engineer for Lucent. It has real engineering chops and sits on a pile of IP; but unless it plans to make the quantum leap from SiPh to CPO, it might find itself shut off from the lion's share of its revenue base.

Western companies account for 90%+ of Innolight's sales. If it were shut out from Western markets, it would be left with the 10% left over made up of domestic China. Our research indicates that may be exactly what's happening. Broadcom has the ability to embed their own version of SiPh into a complete CPO unit, shipping an integrated package that works out of the box. Nvidia, for its part, is building a CPO supply chain that pointedly routes around Chinese suppliers. In March, it committed $4 billion — $2B each into Coherent and Lumentum — paired with multi-year purchase commitments and future-capacity rights, explicitly to expand US-based manufacturing of the optical components its co-packaged systems need. The message is clear: the two firms that will define the CPO era are locking in a supply base that doesn't include Innolight.

Final thoughts

Innolight is, at its core, a Chinese assembler of parts into a device that data centers around the world can't get enough of at the moment. It is a one-trick pony, even if that one trick is extraordinarily profitable right now. This profitability must be weighed against a litany of complications stemming from its dependence on overseas markets in addition to the danger of becoming irrelevant outside China. Do not let Innolight's Chinese identity fool you — the business is highly dependent on a Western capex supercycle that is actively attempting to shut it out, which would leave it with nothing but the sliver of revenue that comes from within China if its supply is not disrupted as well. An investment today is a bet on the short-term profitability of a bridge technology outpacing gradual obsolescence and avoiding upsets to the status quo. That said, it is evident that Innolight is not going out without a fight as it seeks to diversify its customers, suppliers, geographic identities, and to gain a larger beachhead into the supply chain of its very disruptor.

What's next?

Well, that was exhausting. I thought that would take a day or two. It ended up taking more than a week. The FY2025 report alone is over 200 pages of business Chinese. But it was an extraordinary learning experience. In addition to practicing my Chinese (which I'm pleasantly surprised with), I was also going from Traditional to Simplified characters, learning about the Chinese financial system, and trying to wrap my head around the tech all at the same time. I hope I've put out a product that makes sense and taken a concrete step towards building a rare and useful skillset. I can't wait to do it again.

Next up, I'll probably look at Eoptolink. It's the closest Chinese competitor and will show if they, too, are standing under the money fountain or if there is something special about Innolight. I've put in the legwork learning the specialized vocabulary and the general layout of Chinese financial disclosures, so I should be able to cash in on some marginal benefits. Maybe eventually, if I'm consistent, I'll be able to do it without the training wheels.